September 15, 2025, Moscow

HOW TO PREPARE A COMPANY

FOR SUCCESSFUL EQUITY RAISING?*

I. Strategic track. Part 1

This article is a continuation of

“Growth Strategy: How to Increase Value Without Falling Into a Debt Trap” article by ink Advisory.

Past success of the company is important, but investors look not only in the rear-view mirror in their assessment. Its equally important for them to learn how the founders and top managers plan to achieve growth of equity value.

The investment appeal of a company is built on an effective business model, a well-thought-out growth strategy, sustainable and transparent processes, and a strong motivated team. Bringing aboard an investor and having a win-win deal requires comprehensive preparation that covers strategy, operations, corporate governance, and financial transparency. This process takes time and attention to detail, which is why it should begin well before the company reaches out to the investment community.

Bringing in an investor is a strategic step that provides the company with capital for scaling, entering new markets, and driving technological transformation. It also grants access to managerial expertise, business networks, and modern management practices.

A win-win deal with investor means that valuation of the business at entry is favorable for the founder, and at the same time this investor sees enough evidence suggesting an even higher valuation in the future. To get to this point preparation must start long before the investment community.

This is a comprehensive process that includes two separate tracks:

- Strategic track: Defining long-term goals, developing a roadmap for achieving them, and building a financial model that demonstrates the company’s growth potential;

- Operational track: Structuring ownership and accounting/reporting systems, ensuring business transparency, improving the efficiency of business processes, and strengthening management team.

The level of preparedness for the investment process is a great indicator of the company’s maturity. A proper preparation of the company also: (i) helps build trust in the founder and top managers; (ii) reduces perceived risks, associated with the company and the investment;

(iii) strengthens the founder’s bargaining position; (iv) clearly demonstrates that the raised capital will work towards achieving strategic goals and increasing shareholder value.

Components of Strategic and Operational tracks

I. Strategic track

- Market and competitive environment

- Current state of business and financial performance

- Strategy and its implementation roadmap

- Financial modeling and business valuation

- Risk analysis

II. Operational track

- Corporate structure and transparency

- Financial and management reporting

- Legal integrity and regulatory compliance

- Management system

- Business processes and digitalization

- Top management and talent management

- Technologies and innovation

- ESG and reputation

I. Strategic track

When considering investment opportunities, investors evaluate not only past and current achievements of target companies – financial performance, market share, growth dynamics, sustainability of competitive advantages, and the quality of the management team – but also strategic direction.

The key question any investor tries to figure out while analyzing the strategy: “Should I join the founders in executing this strategy and board this ship? Boarding the ship would mean sharing the risks and opportunities with the founders, and if this process is to end in success, the strategy must be convincing and clear, with a resounding Yes! to the question above.

What matters is not only the company’s strategic intentions, but also its ability to translate intentions into concrete actions – building the necessary infrastructure for growth, securing resources, strengthening the team, and maintaining discipline in achieving objectives.

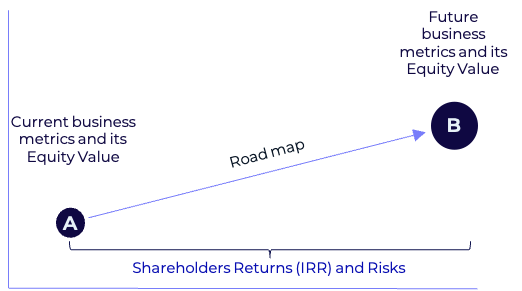

On the one hand, the company must communicate its strategic goals to investors, and on the other hand – present a roadmap describing how it intends to achieve those goals and what resources will be required.

Beyond identifying the sources of growth, the strategy must also address the fundamental questions:

How will this strategy affect shareholder value, and what return (IRR) will it generate for shareholders – both the investor and the founders?

The Goal of the Strategy is to Increase Equity Value and Maximize Shareholder Returns.

The strategy is built through a structured process consisting of five key interconnected components:

- Market and competitive environment analysis

- Assessment of the current state of the business and current/ past financial performance

- Strategy development and creation of implementation roadmap

- Financial modeling

- Risk analysis

Question: How is the market developing, which of its segments are the most promising, and how prepared is the company to compete in them?"

The strategy is authored by the management team jointly with the owner, ensuring a shared vision of the future and forming an investment rationale for the growth strategy.

- Market. The founders usually have a deep understanding of the market: they know the customers, understand the specifics of competition, and monitor market demand trends. These insights are based on years of experience and are precisely what allowed the company to reach significant scale. However, when speaking to investors, observations alone do not suffice. Investors expect to see a systematic and quantitatively validated analysis that demonstrates not only the founder’s expertise, but also the scale of market opportunities.

First step is to clearly define the market in which the company operates and its potential. This is typically done using a three-level model:

- TAM1 – the overall market size, the upper limit of opportunities;

- SAM2 – the portion of the market that the company can realistically serve, given its products and business model;

- SOM3 – the share of the market that the company is capable of and intends to capture in the coming years, based on its strategy and resources.

It is important not to stop at the aggregate SAM figure, but to show its internal structure. Segments may have entirely different drivers, dynamics, and business model requirements. For example, if 60% of the market consists of differentiated products with high margins, this will require the company to have strong infrastructure, a capable team, and investments in brand development. The remaining 40% may be undifferentiated and price-driven, requiring instead cost minimization and high operational efficiency. If the company builds capacity based solely on the total SAM figure, then under conditions of balanced and moderate segment growth it risks underutilizing its newly built capacity.

Such an approach helps investors see that the company thinks systematically: moving from the overall market scale to specific segments where a sustainable business can be built.

However, this alone is not sufficient for assessing prospects. Even at the growth stage, the market splits into segments, each with its own dynamics. For example, in the rigid plastic food packaging market, the segment for dairy products and the segment for fast-food products differ in growth rates, customer structure, and regulatory approaches. Therefore, it is crucial to show investors not only the overall SAM size, but also which segments within it are the most promising, and where the company already has strong positions or knows how to create them.

The next stage of analysis is the market life cycle. For investors, it is important to understand whether the segment is on the growth curve, has reached maturity, or is entering a decline phase. This directly influences strategic logic: whether the focus should be on scaling, consolidation, or searching for new and promising niches.

To provide fuller context, Porter’s Five Forces model can be applied, showing the balance of forces in the industry: how easy it is for new entrants to enter the market, the power of suppliers and buyers, the threat of substitutes, and the intensity of competition within the segment.

And finally, a key element is competitor analysis. Investors want to see not only general market figures but also a clear map of players: leaders of different segments, their strengths, and strategy. It is important to show where the company already has competitive advantages, and where it will need to fight for market share against key competitors. This helps the investor understand in which segments the company plans to strengthen its position, and in which it may take active steps to capture a significant share of the market.

A detailed market analysis allows the founder’s experience and observations to be translated into a language understood by investors. Market data forms the foundation of the investment rationale for the growth strategy: it demonstrates that the company operates in a sufficiently large and promising market, understands the differences within segments, and knows how to assess the sustainability of its position in the competitive environment.

Market information is the starting point that allows the investor to evaluate how well the chosen strategy leverages the company’s competitive advantages, takes into account market opportunities, and addresses external threats.

The Market in the Investment Context

| Element |

What matters to the investor? |

Questions the company must address |

| Market (TAM, SAM, SOM) |

Market size, its boundaries, segments accessible to the company, and target segments |

What are the market size and dynamics – TAM, SAM, and SOM? What data sources were used and why? Which segments are the most promising and why? What technological changes and trends are shaping the market and target segments? |

| Segmentation and growth drivers |

Dynamics of key segments and factors influencing demand |

Which segments are experiencing active growth? What factors drive demand? What opportunities and threats exist? |

| Market life cycle stage |

Assessment of segment prospects: is the market in growth stage, maturity, or decline |

At what stage of the life cycle are the chosen segments? How does this affect the company strategy? What new niches are emerging? |

| Company’s market position |

Current market share, ability to gain and retain a significant share |

In which segments does the company already have strong positions? What is its current market share? Which competitive advantages allow it to maintain these positions? How does the company defend its market share? What are its weak points? |

| Competitive environment and analysis of players |

Intensity of competition and balance of forces among market players |

How intense is competition within the segment? Who are the main competitors? What are their market shares and strategies? What competitive advantages does the company and its competitors have? |

| Industry structure and competitive forces |

Threats of new entrants, substitutes, and the bargaining power of buyers and suppliers |

Is there a threat of new entrants? What are the entry barriers? Is there a risk of substitutes emerging? How strong is the bargaining power of buyers and suppliers? What factors affect industry profitability? |

| Strategic outlook |

Scalability and growth potential of the company in selected markets |

What resources are needed to increase market share? Does the company plan to expand into new segments or regions? What countermeasures might competitors take? |

Question: “Are the company’s key advantages unique enough to sustain its market position in the long run?”

- Current State of the Business and Financial Performance. After analyzing the market, the attention of investors shifts to the company itself: how it is positioned within the market landscape and what results it has already demonstrated. This includes an overview of the company’s current state, its strengths and possible limitations, as well as its ability to scale while taking into account market threats and opportunities.

Investors assess to what extent the company’s chosen strategy relies on its competitive advantages and considers external factors. At this stage, two elements play a central role: business model and historical performance.

- Business model. For the founder, business model is often self-evident: how the company generates revenues, who its customers are, and why they choose its products and/or services. For the investors, however, it is important to present the business model systematically – to show the structure and logic of how value is created and retained.

For the investors, this is not just a diagram of how the business operates, but a tool to understand what drives growth and profitability.

One of the most popular and widely used approaches to describing a business model is the Business Model Canvas (BMC), developed by Alexander Osterwalder and Yves Pigneur¹. This methodology presents business model as nine interrelated building blocks that cover the key aspects of the company – from customer segments and value propositions to cost structure and revenue streams.

A structured description of the business model helps the investor understand: which market segments are being targeted, how the company differentiates itself, and which elements of the business model may require strengthening or transformation in order to scale.

Business Model Canvas (BMC) in the Investment Context

| Element |

What matters to the investor? |

Questions the company must address |

| 1. Customers segments |

Scale and attractiveness of target segments, their dynamics, and diversification of the client base |

What are the company’s main segments and customers? How are sales distributed across segments and regions? Is there dependence on one or several large clients? |

| 2. Value Proposition |

Level of product (service) differentiation, reasons why customers choose them, strength of competitive advantages |

Why do customers choose company products? Which factors are most important for them – price, quality, delivery speed, reliability? What advantages/ barriers protect the company against competitors? |

| 3. Channels |

Effectiveness of distribution and communication channels and their scalability for sales growth |

Through which channels does the company sell its products? Which channels generate the highest share of sales? Which communication channels are the most effective? |

| 4. Customer Relationships |

Long-term relationships and predictability of demand, client retention, and repeat sales |

What share of sales comes from long-term contracts? How does the company retain key clients? What does cohort analysis show regarding retention/ repeat purchases? |

| 5. Revenue Streams |

Structure and predictability of sales, profitability of business lines, pricing policy |

Which products or business lines generate the main sales and margins? How is revenue distributed by segment? How does pricing compare to competitors? |

| 6. Key resources |

Adequacy of capacities, technologies, and human resources to support scaling and operational sustainability |

What are the company’s current capacities and their utilization? How easily can capacity be scaled? What technologies, competencies, and patents underpin the business model? |

| 7. Key activities |

Efficiency of key processes and their scalability |

Which processes are most critical for implementing unique advantages and maintaining competitiveness? Which processes are key for scaling growth? |

| 8. Key partners |

Reliability of the supply chain, diversification of suppliers, and sustainability of partnerships |

Who are the key suppliers and partners? What is the level of dependency on them, and are there alternatives? How does the company manage risks of short-term or long-term supply disruption? |

| 9. Cost structure |

Fixed and variable costs, potential for improving efficiency |

What are the main cost items? What opportunities exist for optimization and efficiency improvement? |

- Historical Performance. The next step is to demonstrate how the company has proven the viability of its business model in practice. An investor evaluates not only the idea or strategy but also the actual results that confirm the company’s ability to grow and generate profit.

Here, the dynamics of key indicators over the last 3–5 years are particularly important. For investors this serves as a kind of “reality check” – whether the business model truly works and is scalable. The main indicators of interest to investors cover several areas.

First and foremost is the scale and dynamics of the business, both for the company as a whole and across business lines and product (or service) groups: sales in monetary and physical terms, gross profit, EBITDA, net income, and their respective margins. What matters to the investor is not just the fact of growth, but its sustainability and predictability, as well as which business segments contribute the most to results.

Equally important is the quality of the client base and the sustainability of demand for the company’s products or services: growth in the number of customers, increase in average ticket size, share of repeat purchases, and the presence of long-term contracts. Cohort analysis is also valuable, as it shows how different groups of customers behave over time: do they stay with the company, increase order volumes, and expand their spending?

Operational efficiency – here the investor sees cost of goods sold and cost structure: direct and variable costs, contribution margin. The efficiency of sales channels and marketing is also reviewed: customer acquisition cost (CAC), customer lifetime value (LTV), and marketing return on investment (MROI). For manufacturing companies, production capacity utilization, defect rates, and product quality are key.

An important area is the company’s financial position, capital structure, and net income: the level of debt and its structure, ability to service obligations, liquidity, and ability to generate free cash flow (FCF). Return on invested capital (ROIC) is analyzed – how effectively the company uses investments to generate profit.

The management system is viewed by investors as the foundation of business sustainability. An experienced management team, clear allocation of responsibilities, transparent reporting, and reliable control mechanisms indicate company maturity and minimize risks when scaling.

Analysis of historical results allows the investors to see in figures and facts the confirmation of the business model’s viability: the company is able to grow, improve efficiency, and manage risks, which builds confidence in its strategy.

Current Operational Results of the Company in the Investment Context

| Element |

What matters to the investor? |

Questions the company must address |

| Scale and business dynamics |

Scale of the business and performance dynamics, sustainability of growth |

How have sales changed over the past 3–5 years: overall and by business lines? Which areas generate the highest sales growth and margins? |

| Customer base sustainability |

Quality and diversification of the customer base, confirming demand stability |

What is the level of customer retention? What share comes from repeat sales? What does cohort analysis show: is the average ticket growing and is retention improving across customer groups? |

| Operational profitability |

Ability to manage costs and scale the business without losing quality and margins |

What measures have been taken to manage cost of goods sold and variable expenses? How have productivity and quality changed? How have CAC, LTV, and ROI evolved? Which channels proved most effective? |

| Financial position, capital structure, net income |

Balance sheet sustainability and ability to generate cash flows for debt servicing and growth, ensuring returns to company owners |

What is the current Debt/EBITDA ratio? What was the Free Cash Flow? Are there liquidity reserves? How efficient is invested capital (IC)? How have net income and profitability changed in recent years? How is net profit allocated? |

| Management system |

Level of company maturity as reflected in completed development projects and management improvements |

What strategic steps have been implemented in recent years? How have they impacted the company’s market position? Which projects have been most effective? What is the quality of the company’s reporting and control systems? Are management decisions data-driven? |

How to prepare a company for successful equity raising? Strategic track. Part 2